Quarterly Playbook - 3rd Quarter 2024

“Silly Season”

[noun]: a period (such as late summer) marked by frivolous, outlandish, or illogical activity or behavior – Merriam-Webster

As we go into the 3rd quarter, we are preparing for a ramp up in the “silly season”. You could argue we have already been in a bit of a “silly season” with the stock market experiencing sky-high valuations amid extreme concentration, the return of “Roaring Kitty” and the first Presidential debate highlighting the upcoming election battle. To add to the silliness, we have seen a very stubborn Fed refuse to lower rates despite inflation gliding steadily lower. When you add all of these ingredients together, you get a recipe for volatility. However, this also provides some opportunity for those that can maintain discipline and resist the urge to chase momentum or sit on too much cash… “Buy not on optimism, but on arithmetic” - Benjamin Graham, author of “The Intelligent Investor”

As we go into the 3rd quarter, we are preparing for a ramp up in the “silly season”. You could argue we have already been in a bit of a “silly season” with the stock market experiencing sky-high valuations amid extreme concentration, the return of “Roaring Kitty” and the first Presidential debate highlighting the upcoming election battle. To add to the silliness, we have seen a very stubborn Fed refuse to lower rates despite inflation gliding steadily lower. When you add all of these ingredients together, you get a recipe for volatility. However, this also provides some opportunity for those that can maintain discipline and resist the urge to chase momentum or sit on too much cash… “Buy not on optimism, but on arithmetic” - Benjamin Graham, author of “The Intelligent Investor”

US Economics

We continue to see a positive but slowing economy as high interest rates have taken their toll. The most recent GDPNow estimate for the 2nd quarter is only at 1.5% after starting the quarter at a 3.9% estimate. This is slightly concerning as the estimate for the 1st quarter was 2.5% and the actual number came in at only 1.4%. The 2nd quarter decrease came mostly from reduced consumer spending via the PCE (Personal Consumption Expenditures) index. Likewise, the Citi Economic Surprise Index is also indicating a slowdown here domestically as well as internationally with both measures below zero, signifying data has been coming in below expectations.

We continue to see a positive but slowing economy as high interest rates have taken their toll. The most recent GDPNow estimate for the 2nd quarter is only at 1.5% after starting the quarter at a 3.9% estimate. This is slightly concerning as the estimate for the 1st quarter was 2.5% and the actual number came in at only 1.4%. The 2nd quarter decrease came mostly from reduced consumer spending via the PCE (Personal Consumption Expenditures) index. Likewise, the Citi Economic Surprise Index is also indicating a slowdown here domestically as well as internationally with both measures below zero, signifying data has been coming in below expectations.

However, the employment picture remains in good shape even with some deterioration. Unemployment has risen to 4.1% as of June for the official U-3 measure vs. 3.8% in March. The U-6 measure (broader definition including part-time) ticked slightly higher as well posting 7.4% in June vs. 7.3% in March. Furthermore, the June labor participation rate fell to 62.6% from 62.7% in March. These are all decent stats in and of themselves, but trending in the wrong direction. The latest JOLTS (Job Opening and Labor Turnover Survey) report shows we are still positively mismatched with more job openings (8.1 Million) than unemployed people (6.8 Million). However, the trend looks like this may reverse in the next 6-9 months. A strong employment backdrop has been key to avoiding recession. Meanwhile, there are more and more signs that lower-income consumers are already experiencing recession-like conditions. While top-earning households account for the majority of consumer spending, lower-income households are pulling back. We believe that’s because high interest rates negatively affect lower-income households much more than others. Lower-income households are more likely to carry balances on credit cards and other

However, the employment picture remains in good shape even with some deterioration. Unemployment has risen to 4.1% as of June for the official U-3 measure vs. 3.8% in March. The U-6 measure (broader definition including part-time) ticked slightly higher as well posting 7.4% in June vs. 7.3% in March. Furthermore, the June labor participation rate fell to 62.6% from 62.7% in March. These are all decent stats in and of themselves, but trending in the wrong direction. The latest JOLTS (Job Opening and Labor Turnover Survey) report shows we are still positively mismatched with more job openings (8.1 Million) than unemployed people (6.8 Million). However, the trend looks like this may reverse in the next 6-9 months. A strong employment backdrop has been key to avoiding recession. Meanwhile, there are more and more signs that lower-income consumers are already experiencing recession-like conditions. While top-earning households account for the majority of consumer spending, lower-income households are pulling back. We believe that’s because high interest rates negatively affect lower-income households much more than others. Lower-income households are more likely to carry balances on credit cards and other  unsecured variable debt which have seen payments rise significantly. In addition, budgets have been squeezed with over 20% cumulative inflation since 2020. This has all led to a decline in inflation-adjusted deposits for the lowest 20% of income earners. That said, this group accounts for less than 10% of overall spending which does not put the overall economy at risk. All in all, we still do not see recession on the horizon. But the risk of a stubborn Fed waiting too long to lower rates and causing growth to fall further below 2% is rising. And that’s just silly….

unsecured variable debt which have seen payments rise significantly. In addition, budgets have been squeezed with over 20% cumulative inflation since 2020. This has all led to a decline in inflation-adjusted deposits for the lowest 20% of income earners. That said, this group accounts for less than 10% of overall spending which does not put the overall economy at risk. All in all, we still do not see recession on the horizon. But the risk of a stubborn Fed waiting too long to lower rates and causing growth to fall further below 2% is rising. And that’s just silly….

US Equity Markets

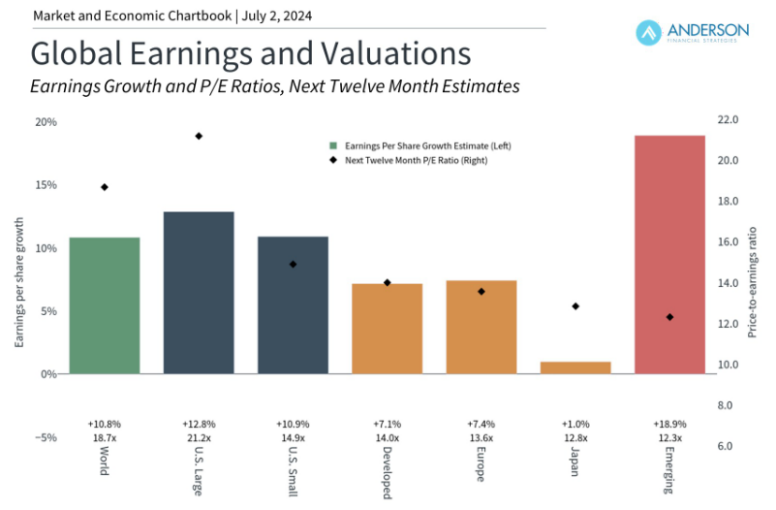

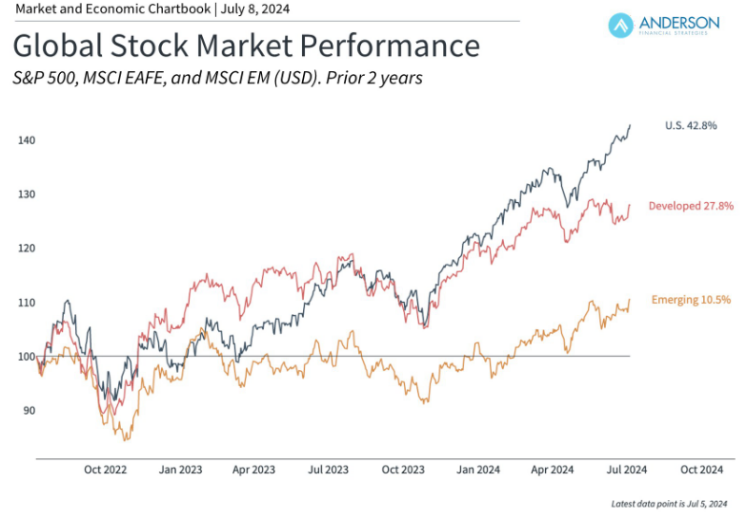

The Stock market currently ranks pretty high on the silly meter. Over a third of the gains in the S&P 500’s 14.5% gain this year are because of a 1 of the 500 stocks, Nvidia. No doubt that Nvidia has put up some impressive earnings in the last 18 months, but with sky-high valuations, it has become the poster child for “believer stocks”. These are stocks that people buy because of some social narrative instead of crunching the numbers. The stock market environment has swung so far that way that even Kieth Gill a.k.a. “Roaring Kitty” is back at it again with Gamestop and others. Meanwhile the Dow Jones Industrial Average that doesn’t include these highflyers is only up 3.8% in the first half of 2024. That said, we have been preparing for a 5-10% correction for the S&P 500 here in the 3rd quarter as the Forward P/E multiple reaches 21X earnings. As you can see from the chart above, when forward P/E multiples reach this high the average market returns for the next 1 year as well as the next 10 years are flat. While the S&P 500 index itself may look extended, we believe there is still opportunity in the lagging areas of the stock market such as Value and Small Caps. We have seen the beginnings of this rotation, but still have a long way to go. At this point, we are only extending our year-end target for the S&P 500 slightly to a high-end of 5,600 while maintaining the low-end of 5,250. This is primarily due to the mainly valuation-led run up that we have seen so far and many of the valuation metrics being at extreme upper values. In our view, one of the biggest driving forces of the markets run-up is the surge in the M2 Money Supply (i.e. circulated currency + money in bank deposits) that happened as reaction to COVID-19 and serves as a sort of back-stop against a higher degree of downward volatilely normally seen in conjunction with high valuations.

The Stock market currently ranks pretty high on the silly meter. Over a third of the gains in the S&P 500’s 14.5% gain this year are because of a 1 of the 500 stocks, Nvidia. No doubt that Nvidia has put up some impressive earnings in the last 18 months, but with sky-high valuations, it has become the poster child for “believer stocks”. These are stocks that people buy because of some social narrative instead of crunching the numbers. The stock market environment has swung so far that way that even Kieth Gill a.k.a. “Roaring Kitty” is back at it again with Gamestop and others. Meanwhile the Dow Jones Industrial Average that doesn’t include these highflyers is only up 3.8% in the first half of 2024. That said, we have been preparing for a 5-10% correction for the S&P 500 here in the 3rd quarter as the Forward P/E multiple reaches 21X earnings. As you can see from the chart above, when forward P/E multiples reach this high the average market returns for the next 1 year as well as the next 10 years are flat. While the S&P 500 index itself may look extended, we believe there is still opportunity in the lagging areas of the stock market such as Value and Small Caps. We have seen the beginnings of this rotation, but still have a long way to go. At this point, we are only extending our year-end target for the S&P 500 slightly to a high-end of 5,600 while maintaining the low-end of 5,250. This is primarily due to the mainly valuation-led run up that we have seen so far and many of the valuation metrics being at extreme upper values. In our view, one of the biggest driving forces of the markets run-up is the surge in the M2 Money Supply (i.e. circulated currency + money in bank deposits) that happened as reaction to COVID-19 and serves as a sort of back-stop against a higher degree of downward volatilely normally seen in conjunction with high valuations.

US Fixed Income

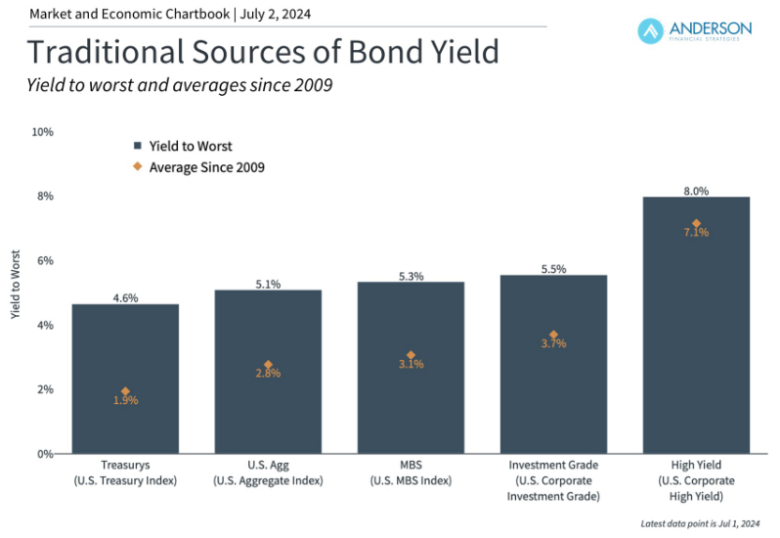

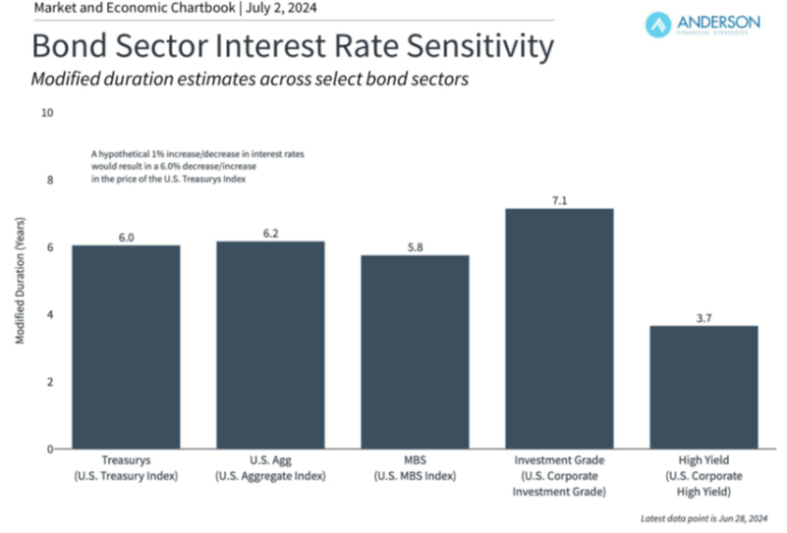

Same story, different quarter with Bonds. The silly season of the market expecting a Fed rate cut but the Fed then delaying has been going on for far too long in our opinion. Nonetheless, this is what the bond markets has been dealt in the first half of 2024. Bonds time will come, however, and this period of outperformnce should commence in the second half of 2024 in our view. Just to reiterate our position, the data we are looking at shows that bonds will likely expereince a period of outperformance over the next two years. As of the mid-year point, bonds are essentally flat for the year. This has challeneged investor patience as Fed rate cuts keep getting delayed. However, even with the delay in starting the process, the Fed is still projecting 2% of rate cuts over the next two years. This means that we are likely to see many areas of bonds generate double digit returns from the combination of starting with higher current yields and benefiting from prices rising due to comparative rates being lower (duration). Many are calling this an opportunity of a lifetime in bonds, but patience and dicipline are being tested as we have seen only a small amount of recovery thus far from the siesmic, 3 standard deviation losses incurred in 2022.

Same story, different quarter with Bonds. The silly season of the market expecting a Fed rate cut but the Fed then delaying has been going on for far too long in our opinion. Nonetheless, this is what the bond markets has been dealt in the first half of 2024. Bonds time will come, however, and this period of outperformnce should commence in the second half of 2024 in our view. Just to reiterate our position, the data we are looking at shows that bonds will likely expereince a period of outperformance over the next two years. As of the mid-year point, bonds are essentally flat for the year. This has challeneged investor patience as Fed rate cuts keep getting delayed. However, even with the delay in starting the process, the Fed is still projecting 2% of rate cuts over the next two years. This means that we are likely to see many areas of bonds generate double digit returns from the combination of starting with higher current yields and benefiting from prices rising due to comparative rates being lower (duration). Many are calling this an opportunity of a lifetime in bonds, but patience and dicipline are being tested as we have seen only a small amount of recovery thus far from the siesmic, 3 standard deviation losses incurred in 2022.

Real Estate

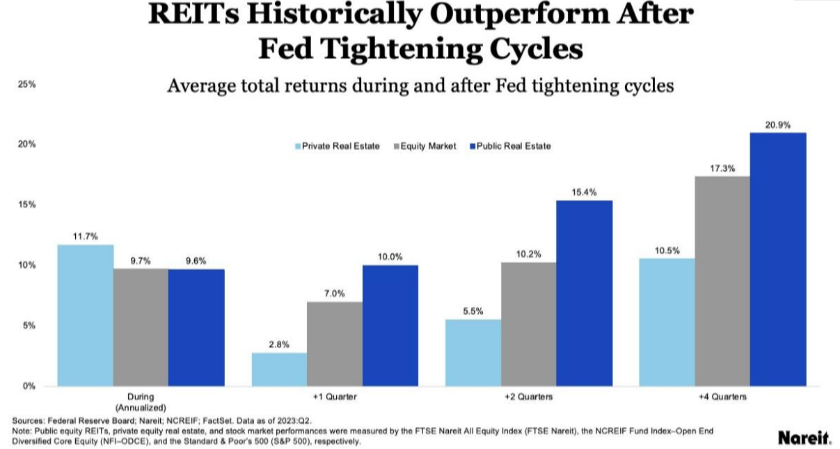

REITs have continued to be plagued by the Federal Reserve playing silly games with delaying interest rate cuts. When those cuts do finally commence, however, the reduction in borrowing costs should benefit listed real estate since it is interest-rate sensitive. In the meantime, net operating income (NOI) has remained healthy and listed real estate valuations are very attractive, especially as a diversifier against an extremely high valued stock market. You can see in the chart that REITs have historically outperformed once the tightening cycle is over. The problem has been, the market hasn’t been able to trust that the tightening cycle has ended quite yet. Overall, the combination of anticipated interest rate cuts, supportive credit conditions, and evolving market dynamics suggest that REITs are well-positioned once interest rates start to decline, and the commercial office space fear overhang is less in the headlines.

Inflation, Interest Rates & the Fed

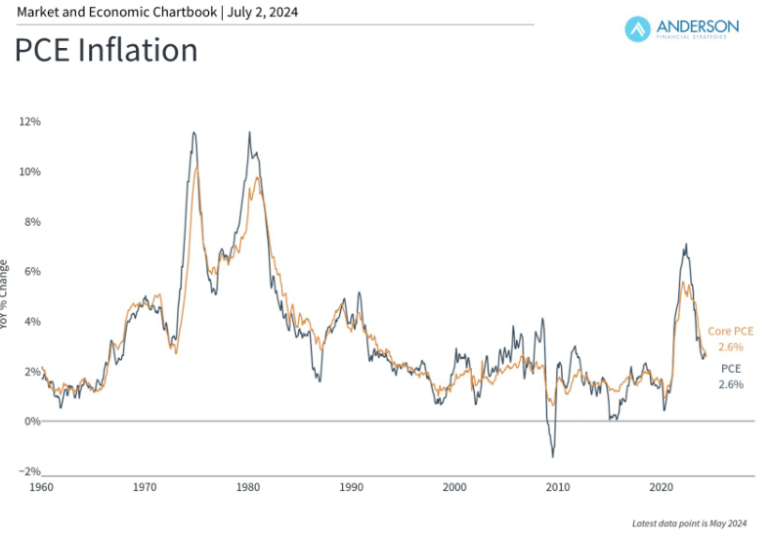

Now THIS is the epitome of silly! Many have been expecting the Fed to have begun to cut rates by now since Core PCE, the Fed’s supposed primary measure of inflation, has been below 3% since December of 2023. Furthermore, this has been steadily declining since peaking in February of 2022 at a year-over-year rate of 5.575% and now sits at just 2.6% with further downward trajectory expected. Now, no one is arguing that rates should be back down to 2% or less, but relieving some pressure is certainly warranted. The last time the Fed kept rates this high for this long some very bad things happened in the economy. Now, we are not saying we are anywhere near the position we were in in 2008. However, the stress of higher rates does take a significant toll. At this stage, we are in the middle of the second longest period in history that the Fed has held rates high, going on 12 months currently. If they wait until September, as the market expects, that will be 14 months.

Now THIS is the epitome of silly! Many have been expecting the Fed to have begun to cut rates by now since Core PCE, the Fed’s supposed primary measure of inflation, has been below 3% since December of 2023. Furthermore, this has been steadily declining since peaking in February of 2022 at a year-over-year rate of 5.575% and now sits at just 2.6% with further downward trajectory expected. Now, no one is arguing that rates should be back down to 2% or less, but relieving some pressure is certainly warranted. The last time the Fed kept rates this high for this long some very bad things happened in the economy. Now, we are not saying we are anywhere near the position we were in in 2008. However, the stress of higher rates does take a significant toll. At this stage, we are in the middle of the second longest period in history that the Fed has held rates high, going on 12 months currently. If they wait until September, as the market expects, that will be 14 months.

The historical average has only been 3 months. This extended period of added pressure has caused lower-income households to experience recession-like conditions, durable goods prices to actually decline, and the housing market to experience a severe drop in the supply of houses for sale and ironically add to inflation. This is not to mention the slow-down effects on the economy and the increased cost of government borrowing. Unfortunately, after being caught off-guard when inflation was accelerating, they seem to be making the opposite mistake by not acknowledging the “meaningful progress” that has been achieved to this point. Nonetheless, they are still in the window of opportunity to be able to correct course without significant negative implications…

The historical average has only been 3 months. This extended period of added pressure has caused lower-income households to experience recession-like conditions, durable goods prices to actually decline, and the housing market to experience a severe drop in the supply of houses for sale and ironically add to inflation. This is not to mention the slow-down effects on the economy and the increased cost of government borrowing. Unfortunately, after being caught off-guard when inflation was accelerating, they seem to be making the opposite mistake by not acknowledging the “meaningful progress” that has been achieved to this point. Nonetheless, they are still in the window of opportunity to be able to correct course without significant negative implications…

Legislative Affairs

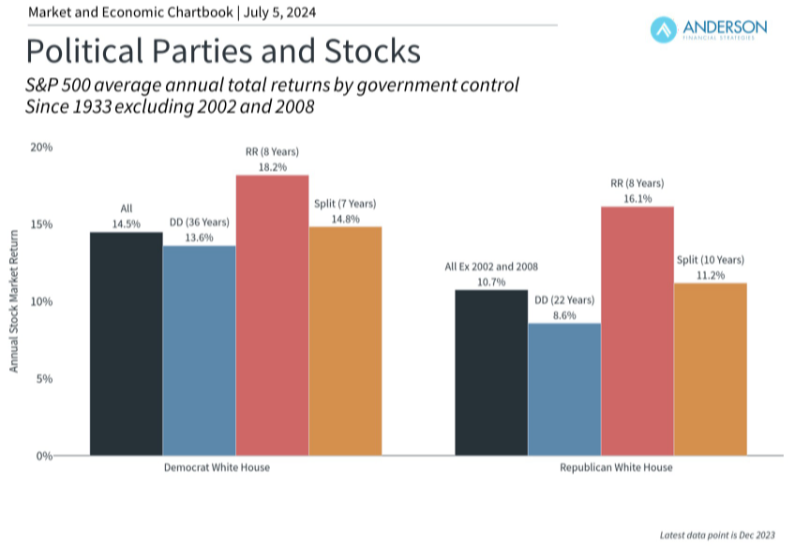

We are now in the thick of it for the silly season of politics, and if there is one thing to remember, it is to expect the unexpected. We thought we knew who the presidential candidates were going to be, but after the first debate between Former President Donald Trump and President Joe Biden, the likelihood of President Biden dropping out has risen significantly. President Biden has fought off challenges from his own party before, so he is still the most likely candidate. However, it does create much more of an unknown scenario. According to the RealClearPolitics Poll average, it appears Former President Trump should win the Presidential election as he has maintained a lead over President Biden for the last six months, with it widening most recently after the debate. The make-up of the House and Senate will certainly have an effect on policy with the Senate likely to be in Republican control as they only need 2 of the 8 “toss-up” races. The House is a bit too early to tell at this point. So what Policy changes could we expect if this occurs:

We are now in the thick of it for the silly season of politics, and if there is one thing to remember, it is to expect the unexpected. We thought we knew who the presidential candidates were going to be, but after the first debate between Former President Donald Trump and President Joe Biden, the likelihood of President Biden dropping out has risen significantly. President Biden has fought off challenges from his own party before, so he is still the most likely candidate. However, it does create much more of an unknown scenario. According to the RealClearPolitics Poll average, it appears Former President Trump should win the Presidential election as he has maintained a lead over President Biden for the last six months, with it widening most recently after the debate. The make-up of the House and Senate will certainly have an effect on policy with the Senate likely to be in Republican control as they only need 2 of the 8 “toss-up” races. The House is a bit too early to tell at this point. So what Policy changes could we expect if this occurs:

The odds of the TCJA (Tax Cuts and Jobs Act) tax cuts for income taxes, business tax reductions and estate tax exemptions getting extended in 2026 goes up considerably.

The odds of the TCJA (Tax Cuts and Jobs Act) tax cuts for income taxes, business tax reductions and estate tax exemptions getting extended in 2026 goes up considerably.- A focus on reducing regulation, especially with electric autos

- Restrictions on energy production likely lifted

- More engagement (and potential volatility) in regards to trade and foreign affairs.

- Renewed enforcement to curb illegal immigration

That said, it is still very early in the silly season of politics and a lot can change between now and November. It is important to remember that markets tend to rally after elections regardless of who the winners are simply because of increased clarity and the desire to “get on with it”….

Financial Planning Corner

Weathering the Changes: A Look at Recent Trends in Property and Casualty Insurance

You don’t want to be silly when it comes to protecting things that matter. When assessing risk there are three options: You can retain the risk, avoid the risk or transfer the risk. When something can be catastrophic but is a rare occurrence often you want to transfer that risk.

By transferring the risk of loss through insurance, you have a safety net in place. The insurance company takes on the financial burden if a covered event occurs. However, understanding what exactly is covered in your policy is key. This knowledge empowers you to plan for situations that might fall outside your insurance coverage.

Recent hikes in property and casualty premiums stem from two main factors: more frequent catastrophic events and rising costs to repair damaged property. In response, many insurers have increased deductibles, adjusted policy coverages, increased premiums and changed how covered items are valued (from replacement cost to actual cash value) after a certain age.

While insurers typically notify policyholders by mail about changes, a yearly review of your policy is crucial. Understanding these updates is key to avoiding surprises. A critical point to examine is whether your coverage is for replacement cost or actual cash value. Replacement cost ensures your home or belongings are rebuilt or replaced at current value, while actual cash value only reimburses the depreciated worth. This difference can be significant, especially for big ticket items such as roofs, cars, and boats.

Keeping the Roof Overhead

The shift from replacement cost to actual cash value for roofs used to happen after 15-20 years, but many insurers have now significantly tightened that window to just 10 years. This means you could face substantial out-of-pocket expenses if your roof needs replacement sooner than expected. Be sure that you know how old your larger covered items are and save for those replacements. Insurance is for the unexpected and not normal wear and tear.

Be mindful that these changes often occur during policy renewals. Insurance companies can't modify the terms of an existing policy mid-term, but they can adjust them at renewal. This means your current coverage might differ significantly from what you had previously. Don't assume your policy remains the same – always carefully review renewal documents.

Don't overlook how rising home values can impact your coverage. Over the past decade, property values have climbed significantly. If your homeowner's insurance is based on a replacement cost from three years ago, it likely won't be enough to rebuild your home today. This could leave you financially responsible for the difference.

Consider adding a buffer to your home's replacement cost coverage. While your insurance covers the rebuild cost up to the policy limit, unexpected expenses can arise after a disaster. Imagine a tornado rips through your town and damages your home. Debris removal, rising labor costs, and inflated material prices can quickly deplete your coverage. A buffer ensures you have additional funds to handle these unforeseen costs and rebuild your home without financial hardship.

Umbrella Coverage

An umbrella policy goes beyond your primary insurance, acting as a powerful safety net. Imagine a lawsuit arising from a serious accident or even a claim like slander. Your homeowner's or auto insurance might have limits that wouldn't fully cover the costs. An umbrella policy kicks in right where your primary coverage stops, shielding you from financial ruin and giving you peace of mind knowing you're protected.

An umbrella policy doesn't just provide extra protection; it can simplify your overall insurance plan. Some insurers require specific coverage levels on your primary policies (like auto and homeowners) to qualify for an umbrella policy. This ensures you have a strong foundation of coverage before adding the umbrella's extra layer of protection.

Life is a journey, and your insurance needs should evolve alongside it. As your net worth grows and you acquire new assets like boats, investment accounts, or even a second home, your insurance coverage needs to adapt. Regular policy reviews ensure your protection keeps pace with your changing circumstances. This proactive approach brings peace of mind, knowing you're financially secure against unexpected events.

Just like your wealth evolves, your insurance needs adapt over time. Regular reviews ensure your policy keeps pace with your accumulating assets and ever-changing risks. Think of it as a financial safety net, catching you if the unexpected throws you off course. Schedule your next review today to solidify your property and casualty coverage and achieve the peace of mind that comes with knowing your valuable assets are protected.